|

Recently in Money and Markets, I pointed out some of the forces that could continue to lift stocks in 2014. Among key factors are record stock buybacks and the growing possibility of a major asset-allocation shift out of bonds, which performed poorly in 2013, and into stocks.

But to make for a balanced assessment, it’s only fair to take a look at what could go wrong with the stock market.

As usual, there is a very long list of potential pitfalls and investor anxieties that could pressure stock prices in 2014. After all, it has been said many times that bull markets “climb a wall of worry.” And there has been no shortage of worry this year, including: the impact of Federal Reserve tapering, a sluggish global economy, higher interest rates, and a slowdown in China and other emerging markets.

|

| There has been no shortage of things to worry about this year. |

Despite those worries, investor behavior seems quite complacent at the moment. Perhaps too complacent.

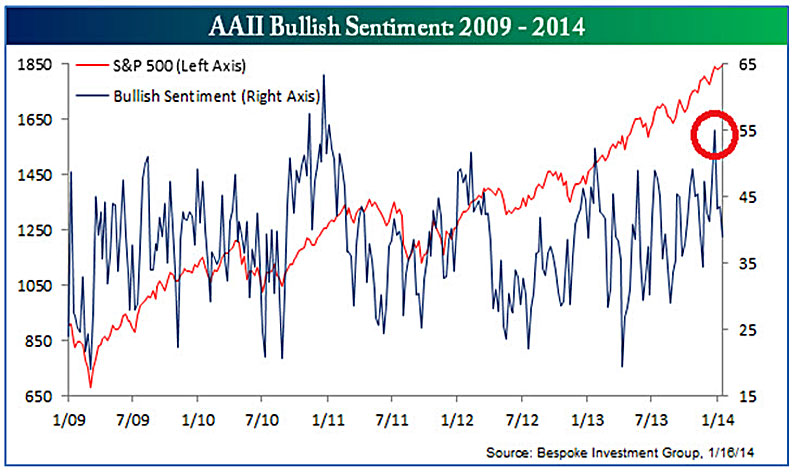

Look at the graph below and you’ll see that 2014 began with retail investors in a very bullish mood, according to poll results by the American Association of Individual Investors.

In fact, it was the most bullish reading in this survey since early 2011. And while stocks meandered through the first half of that year, recall the S&P 500 Index eventually plunged nearly 20 percent from July to October 2011.

More recently, bullish sentiment has declined in this survey, which isn’t surprising with the S&P 500 Index down 3.2 percent so far this year. But several other contrary-sentiment indicators confirm an alarming sense of investor complacency, including the Investors Intelligence Advisory Sentiment Index, which began 2014 at the most bullish extreme since February 1987 … and we all know what happened in October of that year.

Also, my colleague Larry McMillan recently pointed out that the equity-only put/call ratio — a key measure of trading volume in bearish put options versus bullish calls — just rolled over to an extreme low. This means too many bulls (or, if you prefer, too few bears), which can be considered a sell signal for the stock market.

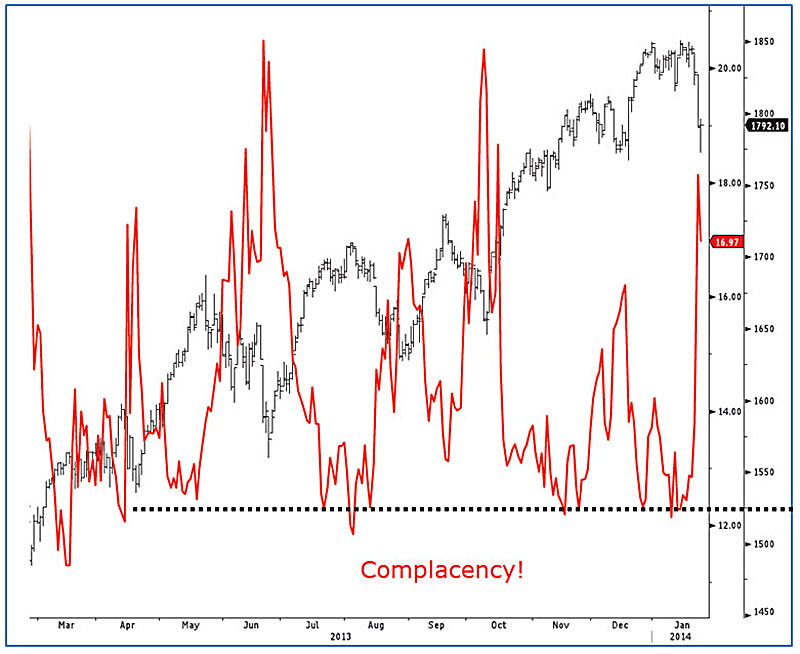

For more confirmation of complacency, just look at the venerable fear gauge itself: the CBOE S&P 500 Volatility Index (VIX) as shown in the graph below.

Just prior to the recent spike higher, VIX traded as low as 12 in late December and again this month. That’s an extremely low reading that had not been registered in six months.

The recent selloff in stocks caused VIX to spike above 18 early this week, another ominous sign for the stock market.

Taken together, these sentiment indicators are a telltale sign of complacency among investors; sentiment simply reached a bullish extreme. Stocks were overbought to start the year and are in need of a correction.

The good news is that over the past three weeks, stocks have indeed corrected and many stocks and sectors are nearing oversold levels now, including one of my favorite industries for 2014: energy.

And the January sell-off has been even more fierce in emerging markets, where many fast-growing countries, which were already cheap to begin with, are even more oversold today.

So there are plenty of longer-term buying opportunities, but the question is, where do we go from here?

In my first Money and Markets column of 2014, I advised you to keep an eye on the first-five-days indicator. Historically, an uptrend over the first five trading days of January is a harbinger of positive returns for the full year; while negative performance is often followed by sub-par annual results.

For the record, the S&P 500 Index was down 0.6 percent over the first five trading days this year (Jan. 2-8). According to this particular indicator, this means the odds of the market ending 2014 with a gain are only about 50/50, compared to a 74 percent chance of an up year when the first five days are positive.

But there’s another early-warning stock market indicator with an even better track record of accuracy: the January Barometer.

According to the Stock Trader’s Almanac, the stock market’s direction in January has correctly forecasted the major trend for the market 81.6 percent of the time. Based on data going back to 1928, whenever the month of January is up, the S&P 500 has posted average full-year gains of 13 percent. But when January is down, the average annual return falls to minus 2.3 percent.

With one day to go until the end of January, the January Barometer is forecasting foul weather.

Good investing,

Mike Burnick

Mike Burnick, with 30 years of professional investment experience, is the Executive Director for The Edelson Institute, where he is the editor of Real Wealth Report, Gold Mining Millionaire, and E-Wave Trader. Mike has been a Registered Investment Adviser and portfolio manager responsible for the day-to-day operations of a mutual fund. He also served as Director of Research for Weiss Capital Management, where he assisted with trading and asset-allocation responsibilities for a $5 million ETF portfolio.

Mike Burnick, with 30 years of professional investment experience, is the Executive Director for The Edelson Institute, where he is the editor of Real Wealth Report, Gold Mining Millionaire, and E-Wave Trader. Mike has been a Registered Investment Adviser and portfolio manager responsible for the day-to-day operations of a mutual fund. He also served as Director of Research for Weiss Capital Management, where he assisted with trading and asset-allocation responsibilities for a $5 million ETF portfolio.